A Business Loan serves as an essential source of funds supporting the operation, expansion and growth of the venture. As an entrepreneur, you get to explore various types of Business Loan in India when in need of money. These variants of Business Loan cater to your specific financial requirements, helping you make the most out of your credit. Read along to learn about these credit types and their features in detail.

9 Types of Business Loans in India

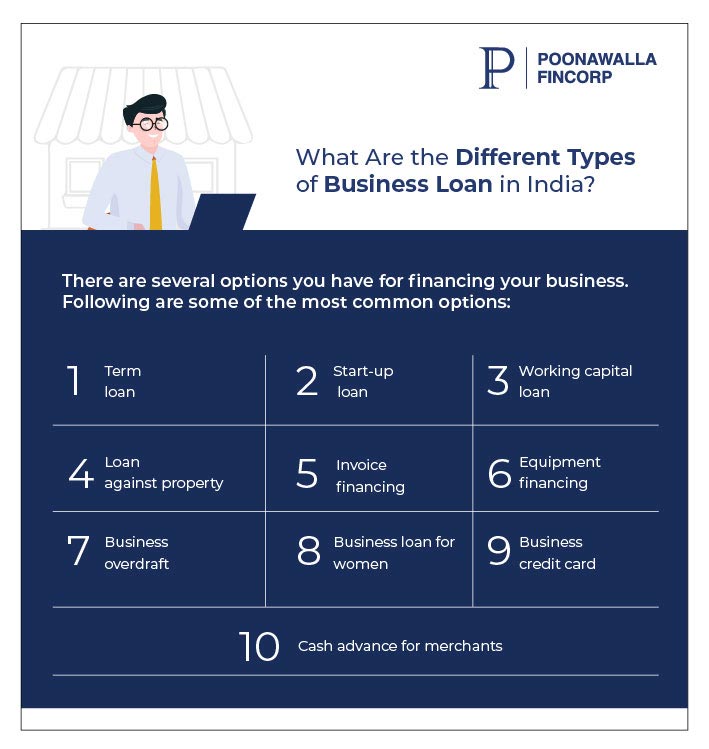

Several variants of a Business Loan are available in the market. Here’s a list of the top 10 types of Business Loan with their unique advantages and disadvantages:

1. Term Loan

One of India's most common types of Business Loan that leading lenders offer is a term loan. The loan amount sanctioned depends on the credit history of the business. Generally, the loan tenure for a term loan is anywhere between 12 months and 60 months.

Pros:

- Larger principal amounts are sanctioned with market-competitive rates.

- Loan amount can be utilised for any business-related expenditure.

- Certain periodical incentives like reduced APRs are extended to existing customers from time to time.

Cons:

- Generally, involves strict eligibility criteria in terms of creditworthiness.

- Lenders ask for an elaborate list of documents to verify all business and personal details.

- The lenders expect two to three years of profitability.

- Although online applications are accepted by most lenders but still the funding times can be long in some cases.

Also Read:

Understanding

Term Loans: A Detailed Guide

2. Working Capital Loan

Enterprises use working capital loans to overcome any kind of financial crunch and meet daily business requirements. The end use of this type of Business Loan can be for managing business cash flow, paying salaries, increasing inventory, purchasing raw materials, investing in machinery/equipment, etc.

Pros:

- Relatively the loan processing times are faster as the money is intended to suffice daily business expenses.

- Usually do not involve collateral

- Relaxed eligibility requirements

Cons:

- Restricted loan amounts

- Typically involves detailed underwriting processes.

- Borrowers are allowed shorter repayment terms.

- Sometimes the overall cost of borrowing can be higher.

Also Read: Boosting Operational Efficiency with Working Capital Finance

3. Loan Against Property

When your business requires a large principal, say a sum of more than Rs. 50 Lakh, you can opt for a Loan Against Property. The borrowers of this type of Business Loan must offer a property as security. Also, the repayment tenures range between 120 months and 240 months.

Pros:

- Much lower interest rates compared to other forms of secured loans

- Provided all the required documents are ready, the processing times are very fast

- You get a long tenure thus the EMIs are easily affordable

- You can apply for a large principal amount

Cons:

- In the event of default, you may lose possession of the property

- Loan amount is restricted and relies on LTV

- A Loan Against Property that come with floating rates can cause greater EMI outflow at times of rising interest

4. Invoice Financing

Invoice financing is suitable for small businesses. When companies face a lag between raising invoices and receiving payments, the Business Loan helps in meeting regular financial requirements. Here, the lender provides funds against the amount raised in the invoice.

Pros:

- Provides quick cash necessary for a business

- Easy approval process

- You, as a borrower, get more flexibility as the lender allows a month or more to return the money

- There is very less risk involved

Cons:

- Some lenders may resort to shady credit policies. However, industry standards have now evolved a lot, encouraging fair transactions

- It may become stressful at times if your client delays in paying the invoice amount

- In the long run, it will lead to reduced profits as the factor company will charge 1-3% of each invoice

5. Equipment Financing

Most manufacturing units require costly equipment for operations. Thus, one of the best types of Business Loan in India for manufacturing businesses is equipment financing or machinery loan.

Pros:

- Fast funding in most cases

- Offers flexible tenures

- Helps build the credit score

- No need for collateral

Cons:

- End usage is specified

- It may be costly if not researched well

- 20% of the equipment’s cost is needed as downpayment

6. Business Overdraft

A business overdraft is a great way to avail quick financing when your venture holds fixed deposits with a particular lender. To approve this loan, the bank or NBFC considers your business’ repayment history, cash flow, fixed deposit terms, and other factors.

Pros:

- Loan terms are flexible, allowing you to borrow only the bare minimum sum

- Processing periods are quicker

- No foreclosure charges

Cons:

- Incurs an arrangement fee in case you wish to extend your overdraft

- You may need to pledge business assets as collateral

- Rates are generally floating in nature. Thus, it is difficult to predict the gross payable interest

7. Business Loan for Women

Some banks and lenders offer a separate financing scheme for women entrepreneurs. The objective is to encourage women who are launching small to medium-sized businesses.

Pros:

- Slightly lower interest rates

- Relaxed eligibility criteria

- Easy online application process

Cons:

- May not be adequately personalised for a particular need

- Documentation needs can be elaborate for some lenders

Also Read: 6 Best Business Loan Schemes for Women Entrepreneurs in India

8. Business Credit Card

To fulfil short-term requirements, a business credit card is excellent. It lets businesses obtain cash when they are in dire need.

Pros:

- Comes with many customer benefits like cash backs, reward points, etc.

- Best for instant access to funds

- Payments become seamless at various points

Cons:

- Interest rates can be much higher compared to other Business Loan types

- Can involve high annual maintenance fees

9. Cash Advance for Merchants

With a merchant cash advance, you can obtain an advance of capital on the daily sales of debit and credit cards. The borrower needs to return the advance with a part of the daily credit sales.

Pros:

- No restrictions on the principal borrowed

- You do not have to pledge anything

Cons:

- Smaller businesses that do not accept credit cards cannot leverage this offer

- It can be more expensive compared to other short-term loans

Best Business Loans for You

When you have a proven track record of running a successful business, obtaining a Business Loan becomes easier. Lenders are confident in your ability to manage your business effectively and repay the loan on time.

So, if you have been running a business for a significant amount of time, the following are the Business Loan types that are most suitable for you:

1. Term Loan

If you are looking for a Small Business Loan, Term Loan can be the most suitable option for you. A Term Loan provides you with the necessary funds to meet your business requirements. These loans come with higher loan amounts and longer repayment tenures. Also, they are provided at competitive interest rates.

2. Line of Credit

A line of credit is a popular type of Business Loan offered by financial institutions. This loan option is preferable in the case of an emergency since it provides you with a credit limit that you can access as needed. Like a business credit card, you can withdraw funds and only pay interest on the amount used.

How to Apply for a Business Loan Online?

From Poonawalla Fincorp, you may apply for a Business Loan by following these steps:

- Step 1: Click on the ‘Apply Now’ button.

- Step 2: Fill out the loan application form using your personal and business details.

- Step 3: Provide the soft copies of the necessary documents and await the loan approval.

To Conclude

It is always prudent to conduct a detailed study on various types of Business Loan in India before selecting the right one for you. By doing this, you can avail financing that is tailored to your business’ profile and requirements. Explore various Business Loan types at competitive rates from Poonawalla Fincorp and take your venture to greater heights!

FAQs

- What is a Cash Credit Facility?

A Cash Credit Facility is a type of short-term loan provided by financial institutions to businesses, allowing them to borrow funds up to a predetermined limit based on their creditworthiness. It provides flexibility for businesses to withdraw and repay funds as per their cash flow needs, making it a convenient source of working capital.

- What is a Bank Guarantee?

A Bank Guarantee is a financial instrument issued by a bank on behalf of a customer, promising to cover the financial obligations of the customer to a third party if they fail to fulfil their contractual obligations.

- What is an MSME loan?

MSME loans are offered to owners of micro, small and medium-sized enterprises. Selected lenders offers these loans both via online and offline to help business owners avail funds of up to Rs. 50 Lakh.

We take utmost care to provide information based on internal data and reliable sources. However, this article and associated web pages provide generic information for reference purposes only. Readers must make an informed decision by reviewing the products offered and the terms and conditions. Loan disbursal is at the sole discretion of Poonawalla Fincorp.

*Terms and Conditions apply